Is a CAP Rate a Good Tool for Small Investment Properties?

Ron Benning (Real Estate Investment Expert)

CA DRE #01058898, eXp Realty of CA.01878277

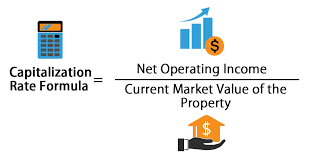

The capitalization rate, or CAP rate, is a commonly used metric for measuring the financial performance of an investment in multi-family residential income property. It is calculated by dividing the property’s annual net operating income (NOI) by its purchase price or current market value. This metric provides a quick and easy way to compare properties’ potential return on investment (ROI).

It is calculated using the following formula:

This article will cover some of the pros and cons of using this analysis tool. The attached video will go into more detail for those who want to use this analysis tool.

Key Advantages of Using the CAP Rate to Evaluate Multi-Family Properties

- It allows investors to compare properties of different sizes and with varying levels of income. For example, a property with a high CAP rate may have a lower annual income but a higher return on investment than a property with a lower CAP rate but a higher annual income. This can help investors identify properties that are undervalued or have the potential for solid returns in the future.

- Another advantage of the CAP rate is that it is relatively easy to calculate and understand. Unlike other metrics, such as the internal rate of return (IRR) or the net present value (NPV), the CAP rate does not require complex calculations or a deep understanding of financial concepts. This makes it accessible to a wide range of investors, including those who are new to the market or do not have a background in finance.

Critical Disadvantages of Using a Cap Rate to Evaluate Small Multi-Family Properties

- It is important to remember that the CAP rate is not a perfect measure of a property’s financial performance. For example, it does not consider the property’s appreciation or rent increase potential, which can be a significant factor in the long-term performance of an investment.

- The most significant limiting factor in using this metric for small investment properties like duplexes and fourplexes is that the operating expenses often need to be more readily available. Additionally, the CAP rate needs to account for the property’s debt service, which can be a high cost for most small investors. Often newer investors need clarification on the fact that a positive CAP rate does not necessarily mean a positive cash flow.

Conclusion

In conclusion, a capitalization rate is a valuable tool for evaluating the financial performance of multi-family residential income properties. Still, it is most suitable for more significant commercial properties where detailed operating data are more readily available. I favor the GRM as a starting point for smaller properties because most small investors use debt, and their actual net income is more critical than the Cap Rate in these circumstances. Once you narrow the properties down to the ones you are most serious about, we recommend running a proforma Cash Flow Analysis to get an annual property operating data report. This report will determine your accurate bottom-line cash flow results. For most small investors, the cash flow numbers ultimately drive their decision. We will cover that topic in our proforma cash flow tutorial.